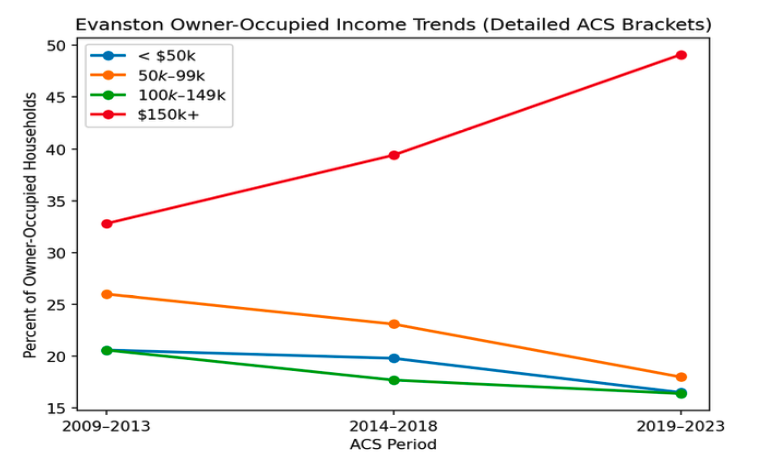

New analysis of U.S. Census Bureau data shows a significant shift in who can afford to remain a homeowner in Evanston. Over the past decade, the share of owner-occupied households earning under $100,000 has steadily declined, while the share earning over $150,000 has grown rapidly. This trend represents a fundamental change in the economic makeup of Evanston’s neighborhoods.

Evanston has long been recognized for its economic diversity, setting it apart from many North Shore communities. The data now show that this diversity is at risk. Without intentional policy action, the city faces the prospect of becoming increasingly accessible only to higher-income households, undermining long-term community stability.

What the data show

• Every income group below $150,000 is shrinking as a share of homeowners.

• The share of homeowners earning over $150,000 has grown dramatically.

• Middle-income homeownership is eroding alongside low-income homeownership.

• These trends are consistent across multiple Census-based income groupings.

Source and Methodology: U.S. Census Bureau, American Community Survey (ACS) 5-Year Estimates, Table B25118 (Tenure by Household Income). Analysis reflects owner-occupied households in Evanston. Income figures are inflation-adjusted. Where custom income thresholds were needed, Census income bins were used directly. Trends are consistent across alternative bracket definitions.

The following letters were written in support of the Evanston local Property Tax Circuit Breaker Program

Dear Councilperson Kelly,

I am writing in support of the proposed Circuit Breaker Program in Evanston, an initiative that would provide meaningful financial relief to residents facing rising housing costs. At a time when too many families—seniors on fixed incomes, long‑time homeowners, and renters—are being squeezed by property tax pressures and the rising cost‑of‑living, this program offers a responsible, targeted, and community‑centered solution. The Circuit Breaker model in Evanston would prevent displacement. This approach protects people from losing their homes because their tax bill grows faster than their paycheck. By tying relief to income, the program ensures support goes exactly where it is needed most—protecting vulnerable residents. Communities across the country have adopted circuit breaker programs because they work. They reduce economic strain, prevent homelessness, and preserve the social fabric of communities. It is a smart, compassionate, and fiscally sound investment in the people of Evanston—one that will provide stability, fairness, and community strength for years to come.

Sincerely,

Kindly,

Laura Fine

State Senator, 9th District

Good afternoon,

As Commissioner Samantha Steele, AAS, of the Cook County Board of Review District 2, I am writing to express my strong support for the proposed Pilot Circuit Breaker Program currently under consideration by the Evanston City Council’s Housing and Community Development Committee (HCDC). This initiative represents a meaningful, targeted step toward providing relief to longtime Evanston homeowners facing rising property taxes—particularly seniors and fixed-income households—who risk being priced out of the communities they have helped build over decades.

The program aligns closely with the mission of the Cook County Board of Review: to ensure fair, accurate, and equitable property assessments while protecting vulnerable residents from undue tax burdens. By creating a local “circuit breaker” mechanism to subsidize or cap excessive increases in property tax bills for eligible long-term residents (such as those with 15+ years of owner-occupancy and meeting income thresholds), Evanston can help preserve housing stability, promote aging in place, and reduce displacement pressures in a high-cost market like ours.

I have reviewed the linked proposal document and appreciate the thoughtful framework it provides. I also want to acknowledge and endorse the three recent amendments you shared with the committee, which would strengthen the program’s integrity, focus resourceson those with the greatest need, and encourage responsible housing choices:

1. Requiring disclosure of significant non-taxable assets (e.g., retirement accounts, additional real property) — This is a prudent safeguard to ensure assistance reaches households with genuine financial hardship, rather than those with substantial hidden resources that may not show on income tax returns alone.

2. Setting a maximum eligible home size of 1,800 square feet (down from the current proposed 2,878 sq ft) — This adjustment better targets modest, affordable homes and supports broader goals of downsizing and long-term housing cost reduction, preventing the program from inadvertently subsidizing larger properties.

3. Modifying the owner-occupancy requirement to 15 consecutive years within the City of Evanston (rather than in the same single home) — This flexible approach recognizes the realities of life changes—such as downsizing for accessibility, health, or family needs—while still rewarding deep community ties. It promotes mobility and right-sizing without penalizing loyal residents.

These modifications enhance the proposal’s fairness, fiscal responsibility, and alignment with anti-displacement priorities. I urge the HCDC Committee to incorporate them as it refines the pilot for full Council consideration.

As a Board of Review Commissioner with over 20 years of experience in property valuation and assessments—including my AAS designation and prior role at the Cook County Assessor’s Office—I stand ready to support Evanston’s efforts in any way possible. This could include providing insights on assessment trends, coordinating with county-level programs (such as senior freeze exemptions or appeal processes), or advocating for complementary state-level reforms to expand circuit breaker protections.

Please feel free to share this letter with all HCDC Committee members, Council colleagues, and relevant staff.

Thank you for championing this important work. Together, we can build a more equitable property tax system that supports our shared

residents and communities.

Sincerely,

Samantha Steele, AAS

Commissioner District 2

Cook County Board of Review

Dear Councilmembers Kelly, Suffredin, and Davis,

I am writing in support of the proposed Property Tax Circuit Breaker Program in Evanston, an initiative that would provide an important and targeted effort to help long-term, low- and moderate-income Evanston residents manage rising property tax burdens and remain in their homes.

As property taxes and everyday expenses continue to rise, many households are finding it harder to keep up. This proposal represents a thoughtful, focused approach to addressing those pressures. This program would provide meaningful relief by limiting the share of property taxes that exceed a sustainable percentage of household income. By prioritizing households with the greatest need and capping individual awards, the program promotes a responsible, targeted, and community-centered solution while extending help to as many residents as possible. Targeting assistance based on income ensures that relief reaches those facing the greatest strain, providing stability for families most vulnerable to being priced out of the community.

The Property Tax Circuit Breaker Program will help prevent displacement, support housing stability, and encourage the economic diversity that makes Evanston a strong and inclusive community. I commend the City for developing a responsible, locally funded solution that addresses affordability without placing new burdens on other taxpayers.

Sincerely,

Robyn Gabel

Majority Leader

State Representative, 18th District

January 20, 2026

Written Testimony to Evanston, Illinois Committee on Housing and Community Development

Members of the City Council’s Housing and Community Development Committee,

Thank you for the opportunity to speak with you today about property tax circuit breakers. My name is Brakeyshia Samms, and I am a senior analyst with the Institute on Taxation and Economic Policy, a nonprofit and nonpartisan research organization that focuses on local, state, and federal tax policy issues with an emphasis on revenue sustainability and tax equity. My testimony will cover how property tax circuit breakers can help with housing affordability. I will also explain how circuit breakers function, summarize major features of programs across the country, and outline important considerations for policymakers.

Circuit breaker credits are the most effective tool available to promote property tax affordability. These policies prevent a property tax “overload” by rebating back property taxes that go beyond a certain share of income. Put another way, this prevents family budgets from being eaten up by property taxes, because circuit breakers ensure that property taxes do not overtake their ability to afford other expenses like groceries, utilities, and car payments.

Currently, state and local governments use a wide array of property tax cuts such as homestead exemptions, tax rate caps, and limits on growth in assessed value. But no tax cut offers a more targeted solution to property tax affordability problems than circuit breaker credits. That’s why I am glad to hear you are considering adopting such a program for the Evanston community.

Other policies fall short on equity when compared to circuit breakers. Homestead exemptions, which exempt a certain portion of home value from tax, are less squarely focused on the issue of property tax affordability, since they usually provide benefits to all homeowners regardless of need. When the exemption is provided as a flat dollar amount, for example, homes worth $400,000 receive the same tax benefit as homes worth $40 million. Percentage-based exemptions are even less equitable, as high-value homes receive the largest benefits.

Capping growth in assessed value misses the mark by an even wider margin. These policies tend to favor wealthier people living in high-value homes that are appreciating quickly in value. Young families seeking to buy their first home fare particularly poorly under assessment caps because artificially holding down the property tax bills of long-time homeowners pushes more of the responsibility for funding local services onto new buyers.

Unlike tax caps or homestead exemptions, circuit breakers measure the affordability of property taxes relative to families’ ability to pay, thus making it a better option and a smart policy choice.

Because property taxes are based on home values rather than income, property taxes are generally disconnected from “ability to pay” considerations in a way that income taxes are not. This disconnect can create problems for families as their financial circumstances evolve. Someone who suddenly becomes unemployed, for example, will find that their property tax bill is unchanged even though their ability to pay it is greatly reduced.

People living in gentrifying areas—a disproportionate share of whom are Black or Hispanic—can also be harmed if their home value and property tax bill surges but their annual income does not keep pace. Your constituents are people of color, low-income, low-wealth, among many other demographics, and a property tax circuit breaker provides a laser-focused solution to the ongoing problem of property tax affordability.

The most common form of help is a threshold-style circuit breaker. Under this approach, credits are calculated using a formula that compares property tax liability to income and offsets some or all the property tax that exceeds what is designated as unaffordable under the program.

The majority of states (29 plus D.C.) offer some kind of circuit breaker, though these policies vary widely in size and scope. Geographically speaking, Illinois is a bit of an outlier for not having a circuit breaker. Both Michigan and Minnesota, for example, have good policies on the books.

Michigan’s program is open to renters and available to households making under $60,000 with property values of $154,400 or less. Their maximum credit is $1,700. In Minnesota it too is available to renters, and homeowners are ineligible after income exceeds $142,490. Their maximum refund of $3,310. The size of the average credit in Minnesota was $1,129 in 2021, which was the latest data available. This could go a long way to helping families afford their property tax bill.

One clear benefit of Minnesota’s policy is that it transforms what would have been a steeply regressive residential property tax into a tax that’s somewhat closer to being flat throughout much of the income scale. This helps contribute to Minnesota ranking among the least regressive overall tax codes, according to our flagship Who Pays report.

Illinois has above-average taxes right now on working class people and a circuit breaker on the city-level is an efficient and targeted way to bring their tax liability down to a more mainstream level. On the whole, Illinois levies what’s commonly called an upside-down tax code. That means the less you make, the more you pay, relative to your income. In our most recent study on this topic, we found that Illinois ranks the 8th most regressive in the country. If that’s concerning you, as frankly I think it should be, a robust circuit breaker is one clear cut way to begin moving in a more positive direction for your constituents.

A circuit breaker is an effective tool to help working-class people afford to stay in their homes. This is a policy that directly speaks to the issues in your community and the concerns of your constituents. Implementing a circuit breaker is a straightforward way to ensure that property taxes are set at levels that Evanston’s families can afford.

Here’s a link to our full report on the topic. Feel free to reach out with questions any time.

Thanks for your time today.

Brakeyshia Samms

Senior Analyst

The Institute on Taxation and Economic Policy

1301 Connecticut Avenue, NW

Washington, DC 20036